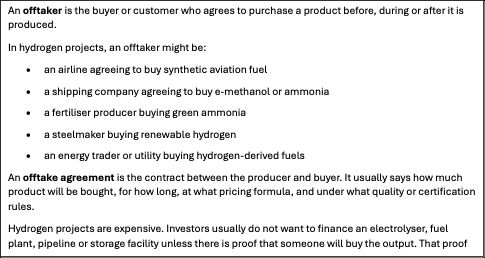

At the edge of Finland’s industrial map, hydrogen is less a gas than a promise moving through pipes not yet built, ports not yet adapted, balance sheets not yet signed, and forests whose carbon may one day be recombined into fuel for aircraft and ships. The molecule itself is simple. The economy around it is not. It asks a country of clean electricity, pulp mills, ports, engineers and cold-water logistics to solve a problem that is becoming familiar across Europe: no one wants to build the supply before demand is firm, no one wants to commit to demand before supply is bankable, and no one wants to finance infrastructure before volumes are visible. VTT’s new HELO project gives this impasse its clearest Finnish formulation. As Jutta Nyblom of VTT puts it, “markets will not commit without reliable supply, companies will not invest without confirmed offtakers, and infrastructure cannot be built without knowing volumes”.

The question, then, is not whether Finland can produce clean hydrogen. In principle, it can. The country’s electricity system is already among Europe’s cleaner ones: Finnish Energy says 96 per cent of Finland’s electricity production was CO₂-neutral in 2025, while Statistics Finland reported that 95 per cent of electricity production in 2024 came from fossil-free sources, with nuclear, wind, hydro, solar and renewable fuels dominating the mix. Nor is the question whether hydrogen has credible end uses. In Europe, policy now points hydrogen-derived molecules towards sectors where batteries and direct electrification struggle, especially steel, chemicals, shipping, aviation and fertilisers. The European Commission’s hydrogen framework, REPowerEU and the revised Renewable Energy Directive have created binding or quasi-binding demand signals for renewable hydrogen and its derivatives, while ReFuelEU Aviation and FuelEU Maritime are beginning to turn regulatory ambition into fuel-market pressure.

The harder question is whether Finland can assemble a whole value chain quickly enough, cheaply enough and credibly enough to capture more of the value than merely hosting electrolysers. That is where the HELO project matters. Announced by VTT in June 2026 and led by VTT and the University of Vaasa, the two-year, EUR 1.46 million project is not framed as a breakthrough in electrochemistry. Its subject is the less glamorous but more decisive layer of the hydrogen economy: logistics. It starts from market demand and works backwards through storage, transport, production and raw materials for hydrogen derivative products such as eSAF, e-methane, ammonia, urea and industrial intermediates.

That makes HELO an unusually revealing project. It suggests that the next phase of hydrogen innovation in the Nordics may not be led by the laboratory alone, but by the spreadsheet, the port authority, the grid planner, the rail terminal, the pulp-mill carbon balance, the shipping contract and the offtake agreement. In other words, Finland’s hydrogen test is now a systems test.

A country with the right ingredients, but not yet a recipe

Finland’s hydrogen case is built on three visible advantages. The first is clean electricity. Electrolytic hydrogen is only climate-relevant if the electricity used to split water is low-carbon and, under EU renewable fuel rules, demonstrably renewable according to strict criteria. Finland’s power mix gives it a stronger starting point than many European competitors, with high shares of nuclear, wind, hydro and biomass-based generation and relatively low system emissions. Fingrid’s real-time emissions tool, for example, calculates the carbon intensity of Finnish electricity production using operational data and specified emission coefficients, while Finnish Energy and Statistics Finland both show the long-term decline of fossil-based electricity generation.

The second advantage is land and wind. Business Finland has presented Finland as one of Europe’s most attractive clean hydrogen locations, saying the country has more than 40 hydrogen investment projects in the pipeline with a combined value of more than EUR 17 billion. It also reports grid connection enquiries for an additional 400 GW of renewable energy, much of it land-based wind power. These numbers should be read cautiously, because grid enquiries are not investment decisions, but they do indicate the scale of industrial speculation now attaching to Finland’s clean-energy geography.

The third advantage is biogenic carbon dioxide. Hydrogen alone is not enough to make synthetic hydrocarbons. To make e-methane, e-methanol or synthetic kerosene, producers need carbon. Finland’s forest industry, bioenergy sector and pulp-and-paper infrastructure create a potentially important stream of biogenic CO₂. The Hydrogen Cluster Finland strategy and roadmap both identify biogenic carbon dioxide as one of Finland’s strategic resources, and Business Finland has similarly linked Finnish hydrogen opportunities to synthetic fuels and carbon-based derivatives.

This combination helps explain why Finnish hydrogen policy has become increasingly confident. Business Finland has estimated that the hydrogen sector could contribute up to EUR 34 billion annually to national GDP by 2035, rising to EUR 69 billion by 2045, and could create more than 60,000 jobs across production, infrastructure and technology development. VTT’s HELO announcement repeats the EUR 34 billion figure as part of the rationale for addressing logistics. The Finnish Hydrogen Cluster’s 2026 roadmap goes further in political tone, arguing that Finland can become “Europe’s most competitive hydrogen economy” by 2035 if government, industry and EU actors move in parallel on markets, clean energy, biogenic CO₂, finance, safety and infrastructure.

Yet this is where investigation must begin. Hydrogen strategies often look persuasive because each individual component appears plausible: clean power, industrial users, export markets, ports, engineers, public support. The difficulty lies in synchronisation. If power is cheap but grid capacity is delayed, the electrolyser waits. If electrolysers are financed but offtakers hesitate, production remains theoretical. If e-fuel producers find customers abroad but lack storage, port handling or certification pathways, export revenue is postponed. If infrastructure is built too early, tariffs become punitive. If it is built too late, producers cannot reach customers. This is not a problem unique to Finland. It is the central coordination failure of the European hydrogen economy.

The bankable market is small

The European hydrogen story has always moved faster in policy documents than in steel and concrete. The EU’s hydrogen strategy and REPowerEU plan set an ambition to produce 10 million tonnes of renewable hydrogen domestically and import another 10 million tonnes by 2030. The Commission now presents renewable and low-carbon hydrogen as part of a broader framework for industrial decarbonisation, transport fuels and energy security. The European Hydrogen Observatory describes the EU strategy as a phased approach, beginning with electrolysers close to existing industrial demand and expanding towards a backbone of hydrogen infrastructure by 2030.

But the International Energy Agency’s evidence is sobering. Its Global Hydrogen Review 2025 says the sector has moved from a handful of demonstrations to more than 200 committed low-emissions hydrogen investments, yet growth has not matched early-decade expectations. The IEA identifies costs, infrastructure readiness and regulatory uncertainty as barriers to deployment. Its 2025 progress dashboard estimated global installed electrolyser capacity at 4.9 GW in 2025, up sharply since 2021 but still far below the implied scale of 2030 policy targets.

The IEA’s later reporting and industry summaries point in the same direction: project pipelines have been cut back, investment momentum has weakened, and delays or cancellations have often been linked to lack of offtake, high costs, technical constraints and regulation. Renewables Now’s June 2026 summary of the IEA’s 2026 review reported that the 2030 pipeline had shrunk by around a quarter from the previous year, with low-emissions hydrogen constrained by high costs, uncertain demand and lack of infrastructure.

This does not mean hydrogen has failed. It means the period of easy announcements is over. The first wave of hydrogen enthusiasm was built on technical possibility, climate necessity and cheap capital. The next wave will be built on contracts. Finland’s HELO project lands precisely at this turning point. Its importance lies in moving attention from “Can we produce hydrogen?” to “Who buys which molecule, in what form, at what price, through which logistics chain, under which regulation, and by which date?”.

The chicken-and-egg problem

VTT’s HELO project is a direct response to the circularity now slowing hydrogen investment. Its working method is telling: begin with demand and work backwards. Rather than assuming that hydrogen production will automatically create a market, HELO proposes to examine specific product chains, logistics requirements, infrastructure needs and regional scenarios. Tampere and Jyväskylä are mentioned as case examples in related project material, and the City of Jyväskylä describes HELO as a project to model high-value product chains and understand how hydrogen value chains can scale from pilots to cost-competitive systems.

That approach is important because hydrogen is not a single market. It is a family of possible markets with different physical and commercial properties. Pure hydrogen is difficult to store and transport because of its low volumetric energy density. Ammonia can carry hydrogen but brings toxicity, cracking and handling issues. Methanol is easier to handle and has maritime potential, but requires carbon and has its own fuel-system constraints. Synthetic methane can use existing gas infrastructure in some contexts, but faces efficiency and methane leakage concerns. Synthetic aviation fuel is strategically valuable but expensive, tightly regulated and dependent on both renewable hydrogen and eligible carbon.

This is why logistics moves from the margins to the centre. A hydrogen economy is not simply a set of electrolysers. It is a chain of conversions. Electricity becomes hydrogen. Hydrogen becomes ammonia, methanol, methane, urea, synthetic kerosene or industrial feedstock. Each step adds equipment, losses, certification requirements, safety protocols, storage needs and contractual interfaces. In a small domestic market, export logistics become decisive; in a large European market, cross-border infrastructure becomes decisive; in regulated fuel markets, compliance documentation becomes part of the product.

The HELO project’s collaborator list also reveals the shape of the puzzle. Publicly mentioned participants include VTT, the University of Vaasa, Metsä Group, Valio, Finnair, Tesi and the City of Jyväskylä, among others. This is not a narrow energy consortium. It links forestry, food systems, aviation, investment, municipalities and research. That breadth is not decorative. It reflects the fact that hydrogen derivatives may obtain their value from sector coupling: forest-industry CO₂ plus renewable electricity plus hydrogen technology plus transport-fuel mandates plus port logistics plus offtake contracts.

The investigative question is whether such coupling can occur fast enough. Finland does not lack potential sources of value. It lacks a guaranteed mechanism by which those sources become synchronised investment decisions.

The clearest demand signal, and one of the hardest products

Aviation is one of the strongest cases for Finnish hydrogen derivatives because the EU has created an explicit policy pull. ReFuelEU Aviation requires fuel suppliers to increase the share of sustainable aviation fuels supplied at EU airports: 2 per cent from 2025, 6 per cent by 2030 and 70 per cent by 2050. Crucially for hydrogen, it also includes a synthetic aviation fuel sub-target of 1.2 per cent from 2030, rising to 35 per cent by 2050.

This matters for Finland because synthetic aviation fuel, or eSAF, can be made from renewable hydrogen and captured carbon. If Finland can combine low-carbon electricity, eligible carbon dioxide and export logistics, it could supply a growing European market that airlines cannot easily avoid. VTT lists eSAF among the promising uses HELO will consider, and the inclusion of Finnair in the HELO ecosystem points towards the strategic relevance of aviation demand.

But aviation also shows why demand signals are not the same as bankable demand. EASA’s 2025 ReFuelEU Aviation technical report found that reported SAF supplied in 2024 was still overwhelmingly biofuel-based, with 98 per cent of SAF coming from biofuels, mainly used cooking oil. It also found that by 2030 EU SAF production could meet the overall 6 per cent target in optimistic scenarios, but synthetic fuels were lagging, with no facilities having reached final investment decision at the time of reporting.

The price gap is also substantial. EASA reported an average 2024 SAF price of EUR 2,085 per tonne compared with EUR 734 per tonne for conventional jet fuel. Synthetic fuels are typically more expensive again. For Finland, this means the aviation opportunity is real but highly sensitive to regulation, penalties, airline willingness to pay, public support, certificates, feedstock eligibility and production scale.

The innovation, therefore, is not merely producing eSAF. It is designing a chain that can turn Finnish inputs into a certified aviation fuel delivered into a regulated European system at a price that survives airline procurement and avoids becoming a stranded prestige project. That is precisely the kind of backwards-from-demand analysis HELO is designed to perform.

Maritime: more flexible, but less certain

Shipping is another plausible market for Finnish hydrogen derivatives. FuelEU Maritime, applied from 1 January 2025, sets maximum limits on the yearly average greenhouse-gas intensity of energy used by ships above 5,000 gross tonnes calling at European ports. The required reduction starts at 2 per cent in 2025 and reaches 80 per cent by 2050 on a well-to-wake basis.

For shipowners, the compliance pathways are diverse: biofuels, e-methanol, e-ammonia, wind-assisted propulsion, energy efficiency, shore power and pooling. This flexibility is useful for the sector, but creates uncertainty for fuel producers. A Finnish e-methanol project may face competition not only from other e-methanol producers, but from biofuel blending, efficiency gains, ammonia strategies, pooling mechanisms and penalty-based compliance. The Mærsk-led methanol wave earlier in the decade gave methanol momentum, but the wider shipping sector remains technologically plural rather than settled.

Still, Finland has a tangible opening. ETFuels announced in February 2026 that its Ranua Näätäaapa e-methanol project had received an investment tax credit of up to EUR 118.6 million from Business Finland. The project is described as producing 110 kilotons’ per year of renewable hydrogen-based e-methanol using Finnish renewable power and biogenic CO₂, aimed at European maritime and industrial markets.

This is one of the more concrete examples of the Finnish hydrogen derivative thesis. It links renewable electricity, biogenic carbon dioxide, industrial-scale fuel synthesis and European demand mandates. But it also illustrates the financing challenge. A project receiving a tax credit of that scale is not automatically bankable; it still depends on power procurement, electrolyser costs, CO₂ capture, synthesis technology, offtake, shipping logistics, certification and long-term fuel-price confidence.

Maritime may be a better early market than aviation because methanol handling is more mature than e-kerosene certification at scale, and because ships have more flexibility than aircraft in fuel-system design. Yet that same flexibility weakens the certainty of demand for any one molecule. For Finland, the opportunity is real, but it is not a guaranteed lane. It is a contest between fuels, ports, regulations and balance sheets.

Fertilisers and food security

The VTT source also points to fertiliser production using ammonia and urea. This part of the hydrogen economy attracts less attention than aviation or shipping, but it may be strategically more important. Ammonia is already a major hydrogen use globally, mostly produced from fossil-based hydrogen. Replacing that hydrogen with low-emissions hydrogen could decarbonise fertiliser supply and reduce exposure to imported natural gas and ammonia.

The presence of Valio and the connection to Valio’s Food 2.0 programme are therefore significant. Hydrogen derivatives are not only transport fuels; they can sit inside food-system resilience. If renewable hydrogen can support fertiliser production, and if biogenic CO₂ can be used in urea or fuel chains, then the hydrogen economy becomes part of agricultural security, not only climate policy. Jyväskylä’s project note explicitly links HELO to aviation, maritime, industry and agriculture, and Valio frames HELO as a project connecting renewable electricity, biogenic CO₂ and industrial expertise to aviation, shipping, industry and food security.

This is where Finland’s security-of-supply argument becomes more credible. After Russia’s invasion of Ukraine and the European energy crisis, infrastructure that reduces fossil import dependence has acquired a strategic value beyond pure emissions accounting. The Nordic-Baltic Hydrogen Corridor is explicitly framed by Gasgrid as part of energy security, market integration and REPowerEU, while Hydrogen Cluster Finland argues that every tonne of hydrogen and e-fuel produced in Finland reduces dependence on imported energy.

Yet fertilisers also expose a different constraint: price. Agriculture is cost-sensitive. Low-emissions ammonia and urea must compete against international commodity supply unless regulation, carbon pricing, procurement policy or security premiums change the economics. In this sector, the chicken-and-egg problem becomes a food-chain problem: farmers cannot absorb unlimited green premiums, fertiliser producers cannot invest without stable demand, and states may be reluctant to subsidise operating costs indefinitely.

Pipelines, ports and the geography of credibility

Finland’s hydrogen opportunity depends heavily on its export geography. Domestic hydrogen demand is unlikely to be large enough by itself to justify the most ambitious production scenarios. That is why pipeline and maritime export infrastructure dominate the strategic discussion.

Gasgrid is involved in several hydrogen infrastructure initiatives. The Nordic-Baltic Hydrogen Corridor aims to develop hydrogen infrastructure from Finland through Estonia, Latvia, Lithuania and Poland to Germany in the early 2030s. Gasgrid says the planned approximately 2,500 km pipeline could transport up to 2.7 million tonnes of renewable hydrogen per year by 2040, based on pre-study estimates. The project moved into a feasibility-study phase in 2025 with EU Connecting Europe Facility support, and the study is expected to continue until spring 2027.

The corridor has also received Project of Common Interest status, and project partners describe it as an attempt to link North-East European production centres with Central European consumption centres. ONTRAS, the German partner, says the feasibility study will assess routing, compressor locations, investment and operating costs, business models and tariffs.

This is crucial. A pipeline is not simply a technical object. It is a market-making instrument. If built, it could convert Finland from a peripheral producer into part of a Central European hydrogen supply system. If delayed or underused, it could become a publicly supported monument to over-optimism. The difference lies in binding shipper commitments, tariff design, storage integration, permitting, cross-border regulation and the sequencing of production and demand.

Parallel to the Nordic-Baltic route, the Nordic Hydrogen Route aims to build cross-border hydrogen infrastructure in the Bothnian Bay region between Finland and Sweden. Gasgrid describes it as a project to create an open hydrogen market in the early 2030s, support green industrialisation and connect producers with consumers. It too has received EU PCI status and CEF support.

These corridors strengthen Finland’s strategic narrative, but they do not remove the chicken-and-egg problem. They enlarge it. Pipeline developers need credible volume forecasts; producers need confidence that tariffs will be competitive; industrial users need assurances of supply; regulators need to allocate cost and risk before the market exists at scale. This is why HELO’s logistics-roadmapping function matters. Infrastructure cannot be planned only from engineering maps. It must be planned from demand scenarios that can be stress-tested.

Ports are equally important, especially for derivatives. If Finland exports e-methanol, e-ammonia or eSAF, ports become chemical logistics platforms rather than simple cargo nodes. Storage tanks, safety zones, bunkering systems, blending infrastructure, customs procedures, certification tracking and emergency response capacity all become part of industrial competitiveness. European policy may create demand, but ports determine whether molecules move.

Where the innovation lies

The most common mistake in hydrogen journalism is to treat innovation as a property of the electrolyser. Electrolysers matter. Catalysts, membranes, stack durability, balance-of-plant design and manufacturing scale all shape cost. But Finland’s emerging hydrogen story shows that the more decisive innovations may be system innovations.

First, there is logistical innovation. HELO’s novelty lies in treating logistics not as an afterthought but as the organising principle of scale-up. Its demand-backwards method asks which products should be made, where, in what form, and how they should be stored and transported. That may sound managerial rather than scientific, but in a hydrogen economy the logistics model is part of the technology package.

Second, there is integration innovation. Finland’s opportunity depends on combining assets that are usually governed separately: electricity grids, pulp mills, CO₂ capture, fuel synthesis, ports, aviation, shipping, fertilisers and regional development. A working hydrogen derivative chain would be an exercise in industrial symbiosis, not merely fuel production.

Third, there is market-design innovation. The hydrogen economy will not emerge from spot markets alone in the early phase. It needs contracts for difference, long-term offtake agreements, certification systems, public procurement, EU mandates, bankable guarantees and tariff structures that share risk without hiding it. The IEA’s repeated emphasis on demand creation, infrastructure and financing shows that market architecture is now as important as production technology.

Fourth, there is materials and safety innovation. Hydrogen poses specific challenges for storage, transport and infrastructure because of its low density and interactions with metals. Wärtsilä’s June 2026 MatH2 consortium, led by VTT and involving Finnish industry, was launched to address hydrogen-compatible materials, embrittlement, corrosion and component reliability. That project sits beside HELO as a reminder that logistics is not only routing and economics; it is also materials science under stress.

Fifth, there is storage innovation. Finland lacks natural geological formations suitable for conventional large-scale gas storage, according to reporting on the HUG project launched by VTT and GTK. That makes constructed storage concepts more important. Storage is not secondary, because hydrogen production from variable renewables and demand from industrial users must be balanced across time.

Finally, there is policy innovation. The EU’s RFNBO rules, ReFuelEU Aviation and FuelEU Maritime are doing more than regulating emissions; they are creating future markets. Finland’s task is to interpret these rules in ways that support investment without building capacity for products that regulation later excludes or consumers reject.

The risk of believing the headline numbers

The EUR 34 billion GDP figure is powerful, but it should not become a substitute for analysis. Such estimates typically depend on assumptions about production scale, export value, domestic value capture, technology exports, multiplier effects and policy continuity. Business Finland’s figure is useful as an ambition marker; it is not evidence that the market will arrive on schedule.

There are at least five reasons to be cautious:

The first is electricity demand. Hydrogen production is electricity-intensive. Business Finland notes that electricity can account for up to 80 per cent of hydrogen production operating costs. That makes Finland’s low-carbon power mix an advantage, but it also means large-scale hydrogen development will compete for grid capacity, wind build-out, permitting resources and public acceptance.

The second is infrastructure timing. The Nordic-Baltic Hydrogen Corridor is still in feasibility work, with studies expected to continue until 2027 and operational ambition in the early 2030s. Until transmission infrastructure exists, Finland’s hydrogen export options rely more heavily on derivatives, local consumption and maritime logistics.

The third is offtake fragility. Across the global hydrogen sector, lack of binding demand has been one of the biggest causes of delay. IEA materials and sector summaries repeatedly identify lack of offtake, high costs and regulatory uncertainty as reasons projects slip or shrink.

The fourth is technology competition. In road transport and heating, hydrogen increasingly looks less competitive than direct electrification in many use cases. Environmental groups such as the European Environmental Bureau argue that renewable hydrogen should be reserved for no-regret sectors where direct electrification is not feasible, warning against inefficient hydrogen deployment that competes with broader power-sector decarbonisation.

The fifth is carbon accounting. Finland’s biogenic CO₂ is a strategic resource, but it must be governed carefully. Using biogenic carbon in synthetic fuels can reduce fossil carbon flows, but the climate outcome depends on feedstock sustainability, capture boundaries, energy inputs, life-cycle accounting and whether the CO₂ would otherwise have been emitted, stored or used elsewhere.

A serious hydrogen strategy must therefore avoid two temptations: dismissing hydrogen because the early market is messy, and overpromising hydrogen because the national opportunity is politically attractive. Finland’s edge will come not from hype, but from disciplined prioritisation.

What should be prioritised?

If HELO is to be more than another roadmap, it should help Finland answer a small number of hard questions.

First: which hydrogen derivatives offer the highest Finnish value capture per unit of electricity? Exporting raw hydrogen may be attractive if pipeline access to Germany becomes available, but derivatives may retain more value domestically by combining power, CO₂, industrial know-how and logistics. HELO’s focus on several derivative products is therefore appropriate, but it needs comparative economics, not a catalogue of possibilities.

Second: where are the earliest bankable offtakers? Aviation has a clear mandate but difficult economics. Maritime has flexibility but less certainty. Fertilisers have security value but price sensitivity. Industrial intermediates may offer more stable demand in clusters. HELO’s demand-backwards method should distinguish policy-created demand from signed demand.

Third: which regions can host integrated chains rather than isolated plants? Jyväskylä and Tampere are being used as case examples in HELO modelling, while northern Finland and the Bothnian Bay region matter for heavy industry and cross-border hydrogen infrastructure. Regional cases should be judged by grid access, CO₂ sources, water availability, industrial heat use, storage, transport links and public acceptance.

Fourth: how should public money be used? Business Finland’s Hydrogen and Batteries programme has a EUR 230 million funding target for hydrogen, batteries and related low-carbon industries, and Finland has also used investment tax credits for large clean-transition projects. Public support should reduce coordination risk and technology risk, not simply socialise private downside in projects without credible customers.

Fifth: how will Finland avoid stranded infrastructure? Pipeline and storage assets require long lifetimes and high utilisation. If demand develops more slowly than expected, early users may face high tariffs or public authorities may face pressure to rescue underused assets. This is why Gasgrid’s ongoing feasibility studies, market surveys and tariff analysis are not bureaucratic preliminaries; they are central to whether the hydrogen economy is financially coherent.

The competitive edge

Finland’s strongest hydrogen advantage may not be any single resource. Other countries have more sunshine, larger domestic markets, bigger ports or more mature gas infrastructure. Finland’s advantage is the possibility of coherent industrial coordination: clean electricity, strong engineering institutions, forest-sector carbon, stable governance, ports, digital competence, and a political culture that can still convene companies, cities, researchers and public financiers around a shared problem.

That is also why failure would be revealing. If a country with Finland’s electricity mix, institutions and industrial base struggles to turn hydrogen into bankable value chains, Europe should take notice. It would suggest that the obstacle is not national ambition but the deeper economics of the hydrogen transition: expensive molecules, uncertain demand, slow infrastructure, and regulatory complexity.

HELO’s value lies in confronting this before too much capital is locked into the wrong assets. Its EUR 1.46 million budget is small compared with the multi-billion-euro hydrogen visions surrounding it. But if it produces credible scenarios, exposes weak links, identifies realistic logistics pathways and clarifies where Finnish firms should not invest, it may be more valuable than another flagship plant announcement.

The project also reframes innovation as a matter of honesty. It asks whether the value chain closes. It asks whether demand is real. It asks whether production sites connect to carbon, storage and customers. It asks whether Finland’s hydrogen economy can survive contact with ports, tariffs, certification, insurance, safety and procurement departments. These are not glamorous questions. They are the questions that decide whether a strategy becomes industry.

The molecule and the map

Hydrogen’s future in Finland will not be decided by the molecule alone. It will be decided by the map: where the wind blows, where the grid can carry power, where CO₂ can be captured, where tanks can be sited, where ships can bunker, where aircraft can refuel, where pipelines can cross borders, and where contracts can connect producers with users.

Europe’s hydrogen market is indeed taking shape, but not as a smooth continent-wide wave. It is forming unevenly, around mandates, industrial clusters, ports, corridors, subsidies and companies willing to sign long contracts for expensive clean molecules. Finland enters this market with real strengths and real constraints. It has clean power, biogenic carbon, industrial competence and a strong policy narrative. It also has distance, logistics gaps, storage questions, uncertain offtake and exposure to a European hydrogen market that is progressing more slowly than early targets implied.

The chicken-and-egg problem is not a slogan. It is the operating condition of the hydrogen economy. HELO’s promise is that it treats the condition as solvable only through systems thinking. Markets, production, infrastructure and offtakers must be designed together, or they may not arrive at all.

The most realistic conclusion is neither triumph nor scepticism for its own sake. Finland has a credible hydrogen opportunity, especially in high-value derivatives linked to aviation, shipping, fertilisers and industrial carbon use. But the opportunity is conditional. It depends on choosing no-regret markets, building logistics before bottlenecks harden, securing real customers, resisting inflated GDP narratives, and treating infrastructure as a shared industrial risk rather than an automatic public good.

In the Finnish winter, every route matters. A fuel is not useful because it exists in a tank; it is useful because it reaches the place where work must be done. Hydrogen is the same.

For Finland, the next innovation is not only to make the molecule. It is to make the route trustworthy.

Source list:

- Amber Grid. (2026, January 21). Nordic-Baltic Hydrogen Corridor Project. https://ambergrid.lt/en/green-gas/hydrogen/nordic-baltic-hydrogen-corridor-project/967 [transport…..europa.eu]

- Business Finland. (2024, December 11). How Finland is shaping Europe’s hydrogen future. https://www.businessfinland.com/news/2024/how-finland-is-shaping-europes-hydrogen-future/ [wartsila.com]

- Business Finland. (2025, November 3). Hydrogen & Batteries: Dual Helix of Decarbonization. https://www.businessfinland.fi/en/services/Programs-and-ecosystems/Programs/hydrogen-and-batteries/[linkedin.com]

- City of Jyväskylä. (2026, June 17). Jyväskylä joins the Business Finland-funded HELO hydrogen economy project. https://elinkeinopalvelut.jyvaskyla.fi/en/news/jyväskylä-joins-the-business-finland-funded-helo-hydrogen-economy-project [iea.org]

- DNV. (n.d.). FuelEU Maritime: Regulation insights & support. Retrieved July 1, 2026, from https://www.dnv.com/maritime/insights/topics/fueleu-maritime/ [cris.vtt.fi]

- EASA. (2025, October 22). ReFuelEU Aviation Annual Technical Report 2025: 2024 in review. European Union Aviation Safety Agency. https://www.easa.europa.eu/en/document-library/general-publications/refueleu-aviation-annual-technical-report-2025 [transport…..europa.eu]

- European Commission. (n.d.). Decarbonising maritime transport: FuelEU Maritime. Retrieved July 1, 2026, from https://transport.ec.europa.eu/transport-modes/maritime/decarbonising-maritime-transport-fueleu-maritime_en [vttresearch.com]

- European Commission. (n.d.). Hydrogen. Retrieved July 1, 2026, from https://energy.ec.europa.eu/topics/eus-energy-system/hydrogen_en [neaman.org.il]

- European Commission. (n.d.). ReFuelEU Aviation. Retrieved July 1, 2026, from https://transport.ec.europa.eu/transport-modes/air/environment/refueleu-aviation_en [transport…..europa.eu]

- European Environmental Bureau. (2023, January). A sustainable hydrogen strategy for the EU. https://renewables-grid.eu/app/uploads/2023/07/Policy-Brief-sustainable-hydrogen-strategy-for-the-EU.pdf[iea.org]

- European Hydrogen Observatory. (2025, December 1). EU Hydrogen Strategy under the EU Green Deal. https://observatory.clean-hydrogen.europa.eu/eu-policy/eu-hydrogen-strategy-under-eu-green-deal [h2cluster.fi]

- ETFuels. (2026, February 23). ETFuels secures €118.6 MM Finnish clean transition tax credit for Ranua e-methanol project. https://et-fuels.com/article-etfuels-finnish-credit [e-fuels.com]

- Fingrid. (n.d.). Real-time CO₂ emissions estimate. Retrieved July 1, 2026, from https://www.fingrid.fi/en/electricity-market-information/real-time-co2-emissions-estimate [gasgrid.fi]

- Finnish Energy. (n.d.). Electricity generation. Retrieved July 1, 2026, from https://energia.fi/en/energy-sector-in-finland/energy-production/electricity-generation/ [ambergrid.lt]

- Finnish Energy. (n.d.). Energy production. Retrieved July 1, 2026, from https://energia.fi/en/energy-sector-in-finland/energy-production/ [nordicbalt…rridor.com]

- Gasgrid Finland. (n.d.). Nordic-Baltic Hydrogen Corridor. Retrieved July 1, 2026, from https://gasgrid.fi/en/hydrogen-development/nordic-baltic-hydrogen-corridor/ [bioenergia.fi]

- Gasgrid Finland. (n.d.). Nordic Hydrogen Route. Retrieved July 1, 2026, from https://gasgrid.fi/en/hydrogen-development/nordic-hydrogen-route/ [et-fuels.com]

- Hydrogen Cluster Finland. (2023, June 27). Clean hydrogen economy strategy for Finland. https://h2cluster.fi/wp-content/uploads/2023/06/H2C-H2-Strategy-for-Finland.pdf [businessfinland.fi]

- Hydrogen Cluster Finland. (2026, January 14). Finnish Hydrogen Cluster’s roadmap released: Europe’s most competitive hydrogen economy is built through joint efforts. https://h2cluster.fi/finnish-hydrogen-clusters-roadmap-released/ [iea.org]

- Hydrogen Cluster Finland. (2026, January). Hydrogen economy roadmap for Finland: Europe’s most competitive hydrogen economy. https://h2cluster.fi/wp-content/uploads/2026/01/Hydrogen-economy-roadmap-for-Finland.pdf [process-wo…ldwide.com]

- International Energy Agency. (2025, September 5). EU Hydrogen Strategy. https://www.iea.org/policies/11721-eu-hydrogen-strategy [cris.vtt.fi]

- International Energy Agency. (2025, September 12). Global Hydrogen Review 2025. https://www.iea.org/reports/global-hydrogen-review-2025 [lowcarbonpower.org]

- International Energy Agency. (2025). Progress summary dashboard: Global Hydrogen Review 2025. https://www.iea.org/reports/global-hydrogen-review-2025/progress-summary-dashboard [fingrid.fi]

- Nordic-Baltic Hydrogen Corridor. (n.d.). Nordic-Baltic Hydrogen Corridor. Retrieved July 1, 2026, from https://www.nordicbaltichydrogencorridor.com/ [hydronews.it]

- ONTRAS Gastransport GmbH. (n.d.). Nordic-Baltic Hydrogen Corridor. Retrieved July 1, 2026, from https://www.ontras.com/en/infrastruktur/innovationsprojekte/nordic-baltic-hydrogen-corridor [easa.europa.eu]

- Renewables Now. (2026, June 18). Low-emissions hydrogen momentum weakens in 2025, IEA. https://renewablesnow.com/news/low-emissions-hydrogen-momentum-weakens-in-2025-iea-1296707/[data.fingrid.fi]

- Statistics Finland. (2025, April 15). Altogether 95 per cent of Finland’s electricity production was based on fossil-free energy in 2024. https://stat.fi/en/publication/cm1kktw8ualm207vwnzpsmpc8 [ontras.com]

- Valio. (2026, June 17). HELO project addresses logistical barriers of Europe’s hydrogen market. https://www.valio.com/articles/helo-project-addresses-logistical-barriers-of-europes-hydrogen-market/[observator….europa.eu]

- VTT Technical Research Centre of Finland. (2022, June 17). A new hydrogen research forum to accelerate Finland’s transition towards a hydrogen economy and enable success in international competition. https://www.vttresearch.com/en/news-and-ideas/new-hydrogen-research-forum-accelerate-finlands-transition-towards-hydrogen-economy [nortonrose…bright.com]

- VTT Technical Research Centre of Finland. (2026, June 17). As Europe’s hydrogen market takes shape, Finland tackles logistical constraints to strengthen its competitive edge. https://www.vttresearch.com/en/news-and-ideas/europes-hydrogen-market-takes-shape-finland-tackles-logistical-constraints [energy.ec.europa.eu]

- Wärtsilä. (2026, June 25). New consortium drives hydrogen adoption through advanced material innovation. https://www.wartsila.com/media/news/25-06-2026-new-consortium-drives-hydrogen-adoption-through-advanced-material-innovation-3766389 [vttresearch.com]